As more transparent cash and payment solutions have emerged, so too have people’s attitudes towards credit cards.

In February 2022 we surveyed more than 1,100 Beforepay customers and found 47% of respondents preferred Pay On Demand™ as their short-term cash solution. This compares to 56.8% who ranked credit cards as their least preferred option.

While credit cards and Pay On Demand™ both offer alternative methods to help with key purchases, customers are turning to Pay On Demand™ as the more cost-effective way to manage temporary cash flow challenges and access fast cash.

Let’s take a closer look at some of the reasons why services like Pay On Demand™ with Beforepay are becoming more attractive to customers.

Pay Advance vs Credit Cards - What Are They?

Beforepay’s Pay Advance was developed as an ethical, customer-friendly way to access cash when you need it for a fixed fee. With a Pay Advance, cash is deposited into your nominated account, and you have the flexibility to use it as you see fit.

Credit cards allow you to make a purchase on credit now, and pay it back later. You can use the card to make purchases at merchants.

Pay Advance vs Credit Card - Limits & Responsible Spending

Credit cards

Credit cards allow you to make multiple purchases on credit, up to the limit provided by the credit card issuer.

This gives you the freedom to use a large sum of credit, as a proxy to money, any time, but also puts you at risk of revolving debt if you don’t pay off your balance in full each month.

As of June 2022, Finder reported that Australians carry an average credit card balance of $2,890, with the national debt estimated to be $18.2 billion.

Making purchases using a credit card is easy. But it also requires you to monitor your spending and stay informed about how your credit card works so you can avoid becoming trapped in a revolving cycle of interest, fees and debt.

Pay Advance

The available amount to cash out on a Beforepay Pay Advance is generally smaller than credit cards.

At Beforepay, this is our way of ensuring you only have access to what you need and can afford to pay back between pay cycles. We do this by assessing a broad range of spending and saving behaviours, as well as previous borrowing and repayment behaviours for existing customers to determine a limit that is personalised to each customer’s circumstances.

And because you can only take out one loan at a time, you don’t ever have to worry about falling into a revolving debt trap.

Pay Advance vs Credit Card - Fees and Interest

Credit cards

Credit cards come with a comprehensive list of fees and charges. These include:

- Annual fees that can range from $29 to $700.

- Late fees that range from $5 to $30 and are charged when you miss your minimum monthly repayment.

- Purchases interest rate that is charged daily when you don’t pay your balance in full and can range from 8.99% p.a. to 24.99% p.a.

- Cash advance fees that cost between 2% and 3.5% of your total transaction.

- Cash advance rate that is charged daily on top of your cash advance fee and usually ranges higher between 19% p.a. and 25.99% p.a.

Additionally, some merchants charge an additional surcharge when you use a credit card.

If you’re able to pay your balance in full each month to avoid interest and fees, credit cards might be a suitable option for you.

If you are only making the minimum repayment every month, you may find yourself in a revolving debt cycle from additional fees and interest charges.

For a general idea of how this might add up, let’s look at a simple example.

Our July 2022 Beforepay Cost of Living Index revealed that the average Beforepay customer spends $66.46 a day across various household expenses. Over a 31-day month, this is a total of $2,060.26.

-1.png?width=1500&name=COL-Index-GRAPHICS%20-%20July%202022%20(1)-1.png)

According to the moneysmart.gov.au credit card calculator, if these expenses are put on a credit card with an interest rate of 20% p.a., and you only make the minimum repayments, with additional interest charges you could end up repaying a total of $8,042 over 25 years and 5 months. This includes $5,982 in interest fees.

The complexity of credit card fees and interest charges can make it difficult to estimate how much you actually owe, and how long you have to keep paying off your debt.

Pay Advance

When you cash out a Pay Advance with Beforepay, you'll know what you owe upfront. Our transparent pricing means any fees and other applicable charges that apply to your loan will be shown to you, so you don't have to worry about nasty surprises and hidden costs.

Customers have also been able to save on late fees with other bills by cashing out a Beforepay Pay Advance to help them pay on time.

In our February 2022 customer survey, 55.3% of Beforepay customers said using Pay Advance as their short-term cash solution has helped them save money on other fees, interest and charges. 28.7% believe they were able to save more than $50.

Putting in the time upfront to compare the applicable fees and charges on credit cards against alternative cash solutions like a Pay Advance might help you save later.

Pay Advance vs Credit Card - Support with Managing Debt

Credit cards

To help customers manage credit card debt, some financial providers offer a balance transfer. This buys you time to pay down your debt by allowing you to transfer your outstanding balance from one credit card to another, and often comes with a low or 0% introductory interest rate for a promotional period.

However, this can end up costing more. In 2018, ASIC reported that 30% of consumers increased their debt by 10% or more after a balance transfer.

This is because your remaining balance could end up accruing interest at an even higher rate if you’re unable to pay off your balance in full within the promotional period.

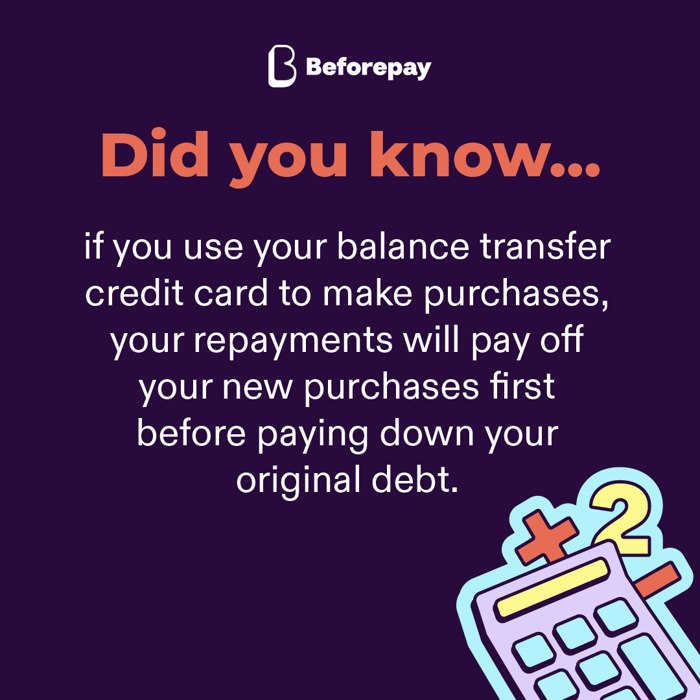

And, if you make new purchases using your balance transfer credit card, any repayments you make will pay off your new purchases first, which will affect your ability to pay down your original debt.

If you take up a balance transfer, review the terms and conditions so you avoid the risk of paying even more in interest.

Pay Advance

Beforepay’s Pay Advance requires you to repay the amount you borrow (including any applicable fees and charges) before you cash out again, ensuring you keep your debt to a minimum.

Pricing is transparent and your repayment schedule is also aligned with your pay cycle, with the option to split your repayments in up to four instalments.

With a Pay Advance, your advance and repayments are managed to help you stay on track with your cash flow and avoid revolving debt.

Saving on credit card fees

While short term loans through services like a Pay Advance with Beforepay offer an ethical, quick and easy option for unplanned expenses, we also understand that credit cards may still be preferred by some people.

Whether you already have a credit card, or are considering one, we still want to help you take care of your financial wellbeing! So here are some general tips for using your credit card to help you avoid paying extra fees and interest.

- Pay your outstanding balance in full every month.

- Make sure you pay by the due date every month, accounting for any processing times and delays (try putting a recurring reminder in your phone).

- Try to limit your credit card expenses and avoid spending your maximum limit every month so you can keep your debt manageable and under control.

- Minimise or avoid taking out a cash advance on your credit card if you can to avoid paying interest on cash advance or a cash advance fee. A cash advance can include ATM withdrawals, gambling transactions, gift cards and prepaid cards, or purchasing foreign currency.

- If you are using a balance transfer, try to limit using the credit card to make any new purchases and pay off your outstanding balance within the promotional period to avoid getting hit by an even higher interest rate on your debt at the end of the promotional period.

Use the moneysmart.gov.au credit card calculator to work out the repayments you need to make to pay off your credit card debt if you are unable to pay your full balance.

Key takeaways

Credit cards and Pay Advances both provide convenient ways to cover your expenses.

Credit cards may be a suitable option for you if you are able to stay on track with your spending and repayments, but come with a greater risk of falling into revolving debt with ongoing fees and interest.

A Pay Advance, like that offered by Beforepay, provides a cost-effective solution if you only need an occasional cash boost. Ensuring you access only what you can afford, one advance at a time, Pay Advance works with you to help you stay in control of your finances.

Whichever you prefer, it’s important to be informed about how each product works and the potential fees and charges that may apply so you can ensure you spend within your means and maintain your financial health and well-being in the long-run.

Find out more about how a Pay Advance with Beforepay works here or tap on the buttons below to open or download the Beforepay app.

Resources

If you or someone you know is experiencing financial hardship or stress, or need help with managing your finances, it can help to speak to someone or refer to various resources for support.

Beforepay Download now

In addition to a Pay Advance the Beforepay app offers a bespoke budgeting tool and personalised spending insights dashboard to help you stay on track of your expenses.

Money Smart moneysmart.gov.au

A source of tools and tips to guide you through taking control of your money.

National Debt Helpline 1800 007 007 ndh.org.au

A free and confidential service with professional financial counsellors who can help you navigate through your debt. Available 9:30am to 4:30pm, Monday to Friday.

Lifeline 13 11 14 lifeline.org.au

For 24/7 crisis support if you are feeling stressed and overwhelmed about your finances.

Disclaimer: Beforepay Group Ltd, ABN: 63 633 925 505. Beforepay allows eligible customers to access their pay and provides budgeting tools. Beforepay does not provide financial products, financial advice or credit products. The views provided in this article include factual information and the personal opinions of relevant Beforepay staff and do not constitute financial advice. Beforepay and its related bodies corporate make no representation or warranty, express or implied, as to the accuracy, completeness, timeliness or reliability of the contents of this blog post and do not accept any liability for any loss whatsoever arising from the use of this information. Please read our Terms of Service carefully before deciding whether to use any of our services.

%20(1).png)

%20(1440x441)%20(1).png)